Insights

2024 Global Technology, Media & Telecom Industry Report

March 29, 2024

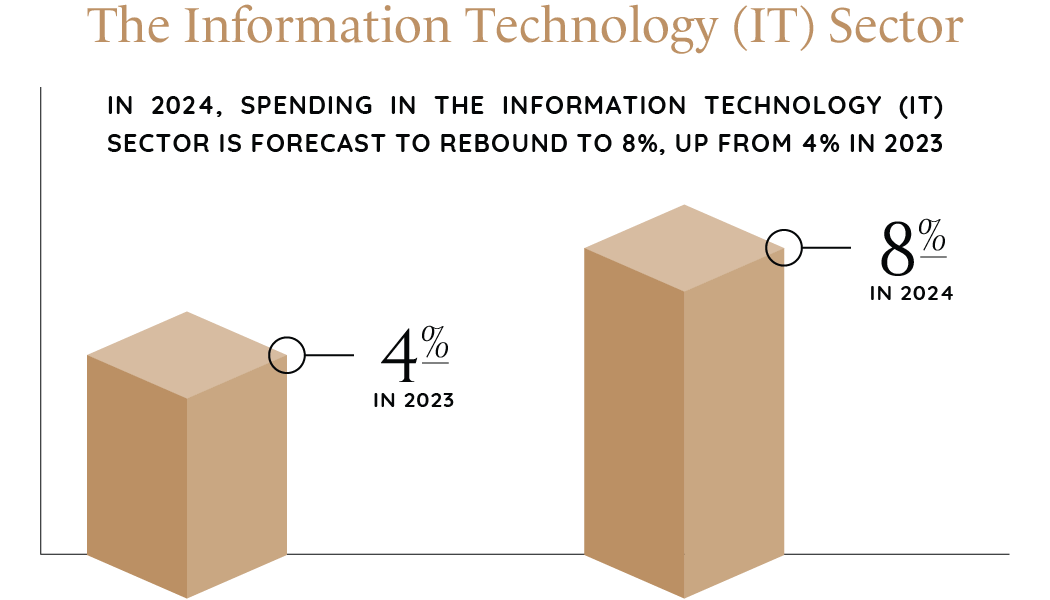

In 2024, spending on the information technology (IT) sector is forecast to rebound to 8%, up from 4% in 2023. The year 2024 will be when the media sector begins to see improved EBITDA and cash flow. Streaming losses are also expected to lessen, improving on a trend that started in 2023. For the telecom sector, stable trends are expected, with moderate growth in earnings, as demand for data remains solid.

Four major players dominate the cloud services segment: Amazon, Microsoft, Alibaba, and Google. No new entrant is expected to significantly disrupt the status of any of these tech giants in 2024, primarily due to the exorbitant cost of capital required to build the necessary cloud infrastructure.

E-Commerce

The pandemic boosted the global e-commerce space to unforeseen levels as brick-and-mortar stores were closed for some time. Tech innovations such as AI, social media advertising, and robotics are helping e-commerce companies retain customers and maintain success. Some key themes shaping the e-commerce sector are the Metaverse, AI, data privacy, supply chain management, and social media.

Industrial Automation

Many companies are seeking to add automation technology because it can play a critical role in helping businesses be resilient. Because automation can supplement human labor, it can be used to offset labor shortages, lower costs, and ease supply chain disruptions. This includes cybersecurity and technologies such as robotics, wearable tech, virtual reality (VR), and augmented reality (AR).

Entertainment & Media

The entertainment and media market grew from $25 trillion in 2023 to $27 trillion in 2024 at a compound annual growth rate (CAGR) of 7.9%. Such historic growth can be attributed to smartphone adoption, social media, streaming services, content personalization, and content globalization.

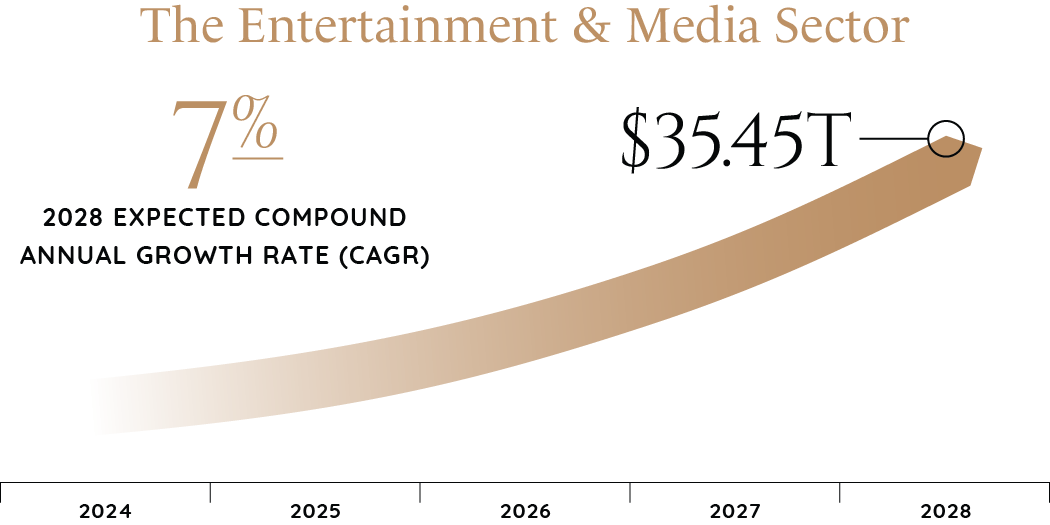

The entertainment & media sector expects to grow to $35.45 trillion in 2028 at a CAGR of 7%. This growth will stem from subscription models, live events, interactive and immersive content, podcasting, sustainability, and regulatory changes. Major influential trends include blockchain in media, AI and machine learning integration, remote production technologies, augmented reality (AR), virtual reality (VR), and the Metaverse. There is also increasing use of over-the-top (OTT) services, driving the market's growth. Over-the-top (OTT) content delivery replaces traditional cable or satellite TV by allowing viewers to stream audio, video, and other media material directly via the Internet, such as Netflix.

Telecom

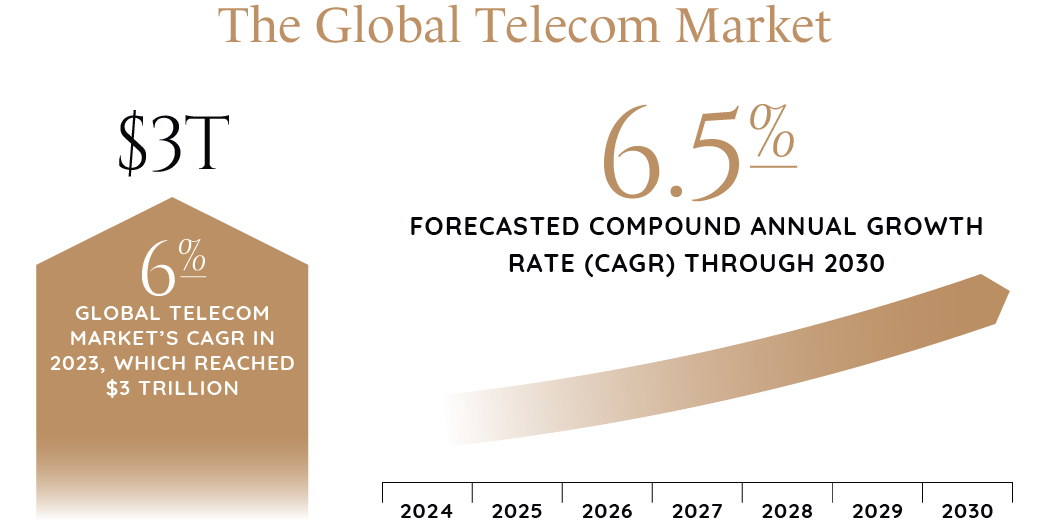

Last year, the global telecom market grew at a CAGR of 6% to reach around $3 trillion, and it is forecast to grow at a CAGR of 6.5% through 2030.

Telecoms are increasingly using bundling strategies to focus on digital services and manage multiple subscriptions to expand revenue and remain competitive. This includes the introduction of various digital services (gaming, health and fitness, utilities, insurance, smart home, etc.) to complement traditional bundles and offer more customization and choice.

Telecom companies are using AI to better manage their cost structures for customer service, HR, and sales while also looking to gain efficiency via task automation. AI is helping to move customers to digital channels such as apps and assisting in network operations. Generative AI is also being used across areas that involve fixed, mobile, and TV. This includes networks, customer service, personalization, and marketing.

Other strategies telecoms are using to stay competitive are new pricing structures and profitability strategies, such as build-your-own plans or do-it-yourself, personalization, and unlimited data plans in select markets.

M&A

In the technology sector, operations are now tighter, and stocks are trading higher. This could lead to an increased appetite for M&A in 2024, especially for smaller tuck-in deals, with harsh regulatory scrutiny resulting in fewer mega deals. While dampened M&A activity for big tech deals is likely to continue, there is optimism surrounding the middle market. Private equity buyers still have record high levels of dry powder ($1.03 trillion in December 2023) and pressure to deploy capital and realize returns could grow from limited partners and investors.

Businesses seeking artificial intelligence strategies will likely translate into increased M&A activity for AI-focused companies.

The media sector continues to undergo digital transformation. Streaming platforms dominate as the primary source of personalized bundles of video, music, and gaming services. Traditional media giants compete against big tech companies for content, advertising, and subscription revenue. Cutting the cord is a key concern for conventional TV, impacting the financials of cable, satellite, and telecom companies. As streaming services and the rise of generative AI shape the industry, consolidation is possible.

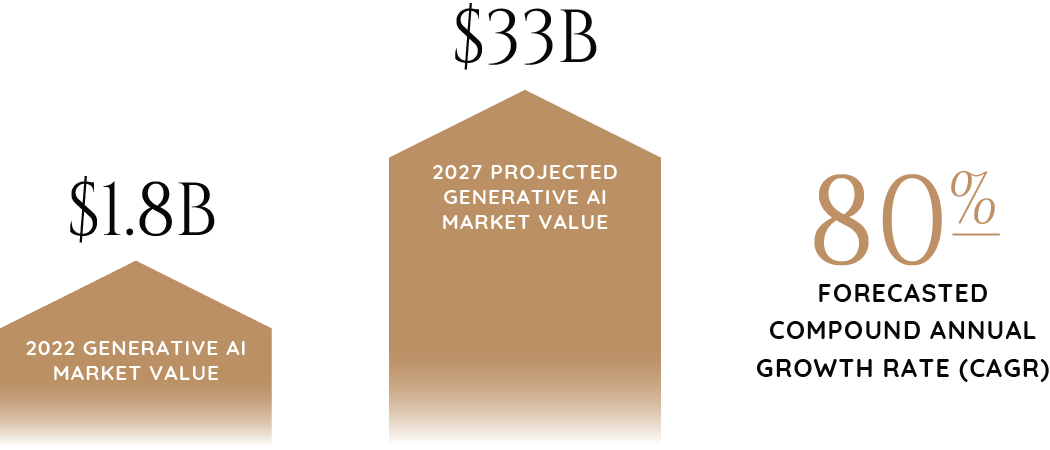

The generative AI market forecasts a stunning compound annual growth rate (CAGR) of 80%, from $1.8 billion in 2022 to $33 billion by 2027. Generative AI is the fastest growing and will account for 10.2% of the overall AI market in 2027 (estimated to be worth $908.7 billion in 2030). This will drive more opportunities for consolidation.

Explore our curated collection today and stay ahead of the curve in M&A.